Executive Summary

XRP, launched in 2012 by Jed McCaleb, David Schwartz, Arthur Britto, and Chris Larsen, originated from Ryan Fugger’s earlier RipplePay concept.1 Designed with a fixed supply of 100 billion tokens, XRP powers the XRP Ledger (XRPL), emphasizing fast, low-cost, and scalable transactions.2

XRP’s main use case is as a bridge currency for cross-border payments via RippleNet and On-Demand Liquidity (ODL). It has been adopted by institutions like SBI Remit, MoneyGram, Santander, and Tranglo, while retail adoption is supported by BitPay and the growing XRPL ecosystem, including decentralized exchanges, non-fungible tokens (NFTs), and tokenization projects.

The XRP token supply is managed through a combination of fixed issuance, a cryptographically secured escrow system, and controlled programmatic and institutional sales. The escrow system, introduced in 2017, ensures predictable monthly releases of XRP, while programmatic sales provide liquidity and institutional sales support strategic use cases.3

Ripple has faced legal challenges, most notably the SEC lawsuit alleging unregistered securities offerings. Partial victories regarding programmatic XRP sales by Ripple have set important regulatory precedents.4 As of August 2025, the SEC’s five-year lawsuit against Ripple concluded with both parties dropping appeals, Ripple paying a $125 million civil penalty, and XRP legally recognized as a security only in institutional sales, providing regulatory clarity in the US.5

The XRPL continues to demonstrate high network activity, processing thousands of transactions per second with a decentralized validator network, supporting a growing ecosystem of applications and institutional use cases. XRP’s combination of technological efficiency, predictable supply, and adoption in global payments makes it a distinctive digital asset in the cryptocurrency landscape.

Founders and Launch

The origins of XRP trace back to 2004, when Canadian developer Ryan Fugger created RipplePay, a decentralized payments platform based on trust lines and peer-to-peer credit.1 RipplePay operated for several years as an alternative payments network, but its adoption remained limited. By 2011, Fugger began discussing the idea of handing the project over to a team that could expand it into a global payment protocol.1

In 2011, Jed McCaleb, best known as the founder of cryptocurrency exchange Mt. Gox, began developing a new digital currency system that didn’t rely on Bitcoin’s proof-of-work mechanism. He recruited David Schwartz, Arthur Britto, and Chris Larsen to help design and build what would become the XRP Ledger (XRPL). This new system used a consensus mechanism that allowed for faster and cheaper transaction settlement compared to Bitcoin, and was designed with a fixed supply of 100 billion XRP tokens.2

In early 2012, McCaleb and the team approached Ryan Fugger with the proposal to merge RipplePay with their new ledger. Fugger agreed, transferring stewardship of the Ripple name and concept to them. Later that year, McCaleb and Larsen co-founded OpenCoin Inc. to commercialize the technology and expand its use. Upon launch, the entire 100 billion XRP supply was created and allocated: 80 billion XRP went to OpenCoin for development and distribution, while the remaining 20 billion XRP was divided among the founders.2

By 2013, OpenCoin rebranded to Ripple Labs Inc., signaling a shift toward enterprise adoption and global payment infrastructure.1 Ripple Labs began distributing XRP to developers, early adopters, and businesses, positioning it as a bridge currency for efficient cross-border payments. This period marked the formal establishment of the XRP Ledger ecosystem and the beginning of its integration into the broader financial landscape.

Uses Cases and Adoption

XRP has been positioned primarily as a bridge currency for cross-border payments, aiming to make international money transfers faster, cheaper, and more efficiently than traditional systems like SWIFT. Ripple Labs built its core products, first RippleNet and later On-Demand Liquidity (ODL), around this use case. ODL allows financial institutions to use XRP as a real-time liquidity tool, converting fiat currency into XRP, sending it across borders in seconds, and converting it back into local currency on the other side. Traditionally, banks have to keep money sitting in special accounts overseas (called nostro/vostro accounts) to make international payments. This ties up cash and slows down settlement. Using XRP, banks do not need to pre-fund those accounts anymore. Payments can be settled instantly, within seconds instead of days, freeing up capital and speeding up transactions. Early adopters of Ripple’s payment technology included SBI Remit, Santander, and MoneyGram, which piloted XRP-based settlement corridors between the US and Mexico in 2019.

Over time, XRP’s use cases have broadened beyond traditional remittances. Ripple has focused on expanding ODL into new corridors, particularly in regions with inefficient legacy banking infrastructure. By 2021, ODL was live in multiple corridors across Asia-Pacific, Europe, Africa, and Latin America. For example, Tranglo, a major payments processor in Southeast Asia, partnered with Ripple to power remittances in markets like the Philippines and Malaysia. Similarly, in 2022, Lemonway, a French payments provider, began using RippleNet for treasury payments in Europe. These integrations highlighted XRP’s growing role in institutional and B2B payment flows.

In addition to financial institutions, XRP has seen limited but notable adoption in retail and commerce. XRP is supported by major payment processors like BitPay, enabling merchants to accept XRP as a form of payment. It is also available at cryptocurrency ATMs in dozens of countries, giving users more accessible on and off ramps for XRP holdings. While merchant adoption has not been as widespread as Bitcoin or stablecoins, these integrations demonstrate XRP’s flexibility as a payment asset.

The developer and Decentralized Finance (DeFi) ecosystem around XRP has also begun to grow in recent years, especially with the introduction of sidechains and interoperability tools. Ripple has supported development on the XRPL, which supports native decentralized exchange (DEX) functionality and issued assets. Projects have emerged using XRP for liquidity, tokenization, and micropayments. For example, the XRPL Grants program has funded open-source projects building wallets, NFT platforms, and payment solutions. Ripple has also launched Ethereum Virtual Machine (EVM) compatibility through its sidechain initiatives to attract developers from other ecosystems.

Adoption has also been visible at the enterprise and government level, particularly outside the US, where regulatory clarity has been stronger. In Japan, Ripple’s long-standing partnership with SBI Holdings has led to deep integration with local remittance services and exchanges. In 2023, Ripple announced collaborations with central banks on CBDC pilots, including work with the Central Bank of Montenegro to explore blockchain-based national currency solutions. These initiatives indicate that XRP and the XRPL are being positioned as infrastructure for both private and public sector financial innovation.

Taken together, XRP’s use cases and adoption span institutional payments, retail commerce, developer ecosystems, and early government partnerships. While its most successful and mature use case remains cross-border settlement through ODL, its ecosystem has steadily diversified over the past decade. The combination of fast settlement, low transaction costs, and growing global partnerships has established XRP as a key infrastructure asset in certain financial corridors, even as regulatory uncertainty has tempered its expansion in the US.

Token Supply

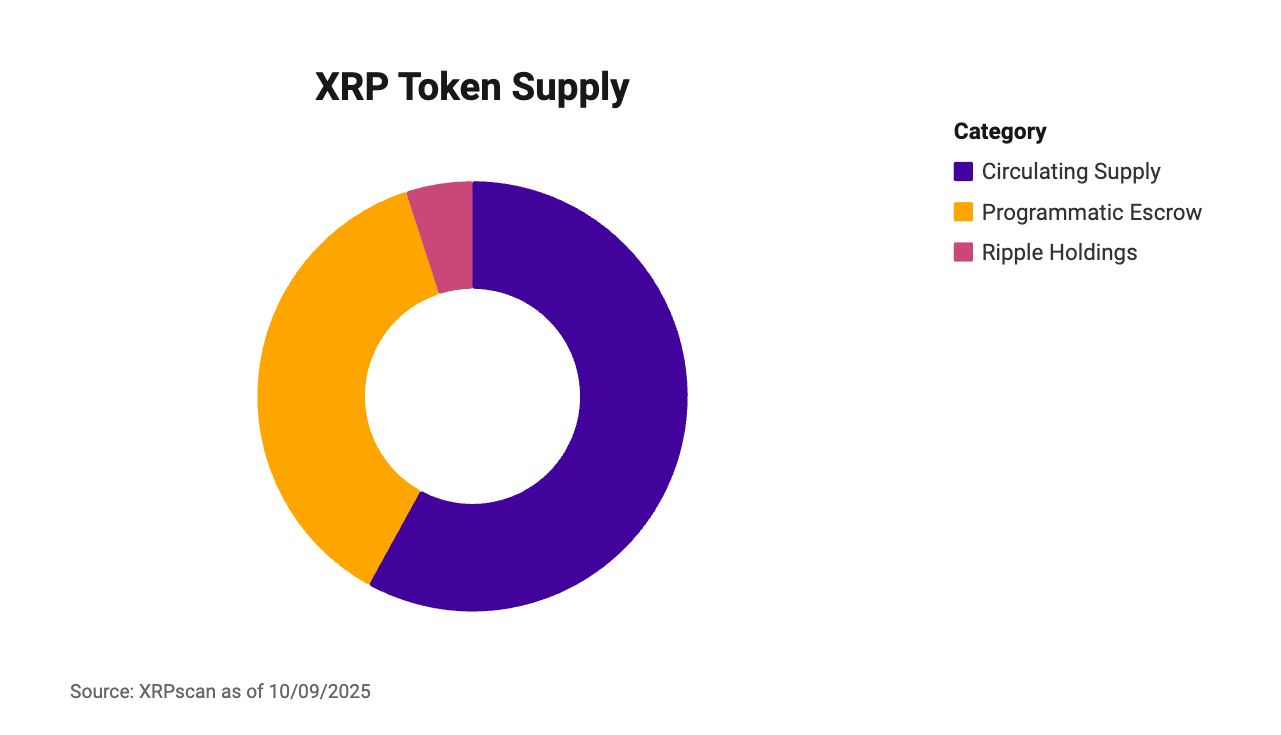

XRP’s token supply dynamics are defined by its fixed total supply, long-term escrow system, and structured distribution through both programmatic and institutional sales. Unlike Bitcoin or Ethereum, XRP has no mining or ongoing issuance; the entire supply was created at launch in 2012. This structure meant that future changes to XRP’s circulating supply would depend entirely on how Ripple and the founders managed and released their holdings over time.2

In December 2017, Ripple introduced a major change to improve supply transparency by placing 55 billion XRP into a cryptographically secured escrow. This escrow system was designed to provide predictability and market assurance. It consists of 55 separate contracts, each holding 1 billion XRP, set to expire monthly over a 55-month schedule. At the start of each month, one contract unlocks, releasing 1 billion XRP. Ripple can use some or all of the unlocked tokens for sales or ecosystem initiatives, and any unused XRP is returned to the escrow, effectively extending the schedule. This mechanism prevents Ripple from releasing large amounts of XRP suddenly and establishes a controlled, time-based release structure.

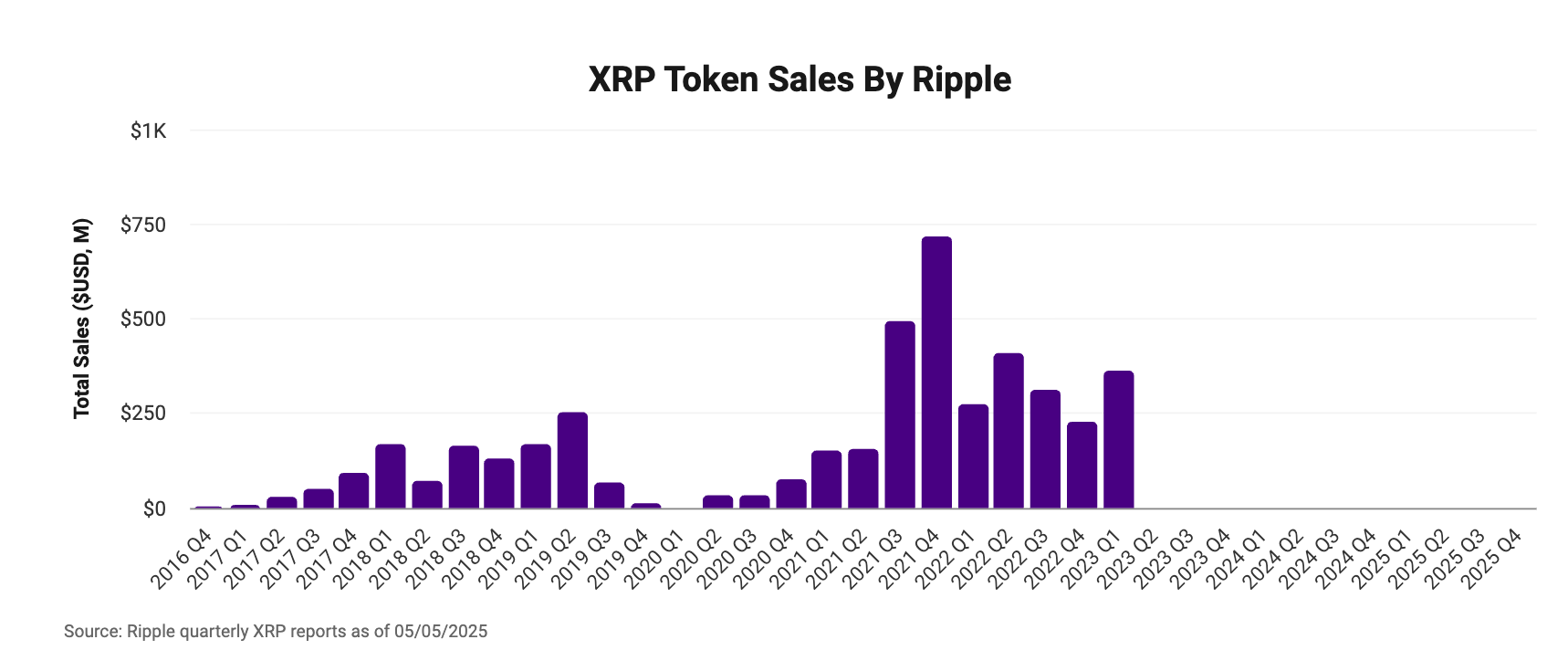

Ripple has historically distributed XRP through two primary channels: programmatic sales and institutional sales. Programmatic sales were automated transactions conducted on public exchanges, typically representing a small percentage of total trading volume. Their purpose was to improve market liquidity and broaden the token’s distribution. Ripple paused these programmatic sales in late 2019 as regulatory uncertainty increased. Institutional sales, by contrast, involve direct over-the-counter transactions with institutional counterparties. These are often tied to Ripple’s On-Demand Liquidity (ODL) product or strategic partnerships and can involve larger volumes. The SEC later focused on these institutional sales in its lawsuit against Ripple, arguing that some of them constituted unregistered securities offerings when made to US investors.4

XRP’s circulating supply expands gradually as Ripple releases tokens from escrow and distributes them through these sales, grants, or ecosystem programs. When Ripple returns a significant portion of unlocked tokens to escrow, supply growth slows. In contrast, during periods of strong demand or market optimism, increased institutional sales can accelerate circulating supply growth. This structure gives Ripple a meaningful degree of control over the pace and scale of new XRP entering the market, which can influence liquidity conditions.

As of 2025, the escrow mechanism remains active, with monthly unlocks and relocks continuing to shape the supply curve. Programmatic sales remain paused, but institutional sales have resumed, focusing primarily on international corridors and use cases tied to ODL. A substantial portion of the total XRP supply remains either in escrow or in Ripple’s treasury, meaning future supply dynamics are still closely linked to Ripple’s release strategy. This combination of fixed supply, predictable time-locked releases, and centralized distribution has made XRP’s supply model both unusually transparent and a source of ongoing debate regarding issuer influence.

Regulatory Challenges

Ripple’s legal challenges in the United States have been a defining part of its history, shaping both its regulatory posture and its reputation within the broader cryptocurrency industry. One of the earliest points of friction came in 2015, when Ripple Labs reached a settlement with the US Financial Crimes Enforcement Network (FinCEN) and the Department of Justice over alleged violations of the Bank Secrecy Act. Regulators argued that Ripple had failed to register as a money services business and had not implemented adequate anti–money laundering measures. Ripple Labs agreed to pay a $700,000 fine, register with FinCEN, and enhance its compliance procedures. This marked the company’s first major regulatory confrontation and pushed Ripple to formalize its approach to financial oversight.

For several years afterward, Ripple largely avoided major public legal disputes, though it continued to face private lawsuits from investors alleging that XRP constituted an unregistered security. These cases were mostly isolated and did not significantly affect Ripple’s operations.

That changed dramatically in December 2020, when the US Securities and Exchange Commission (SEC) filed a high-profile lawsuit against Ripple Labs, CEO Brad Garlinghouse, and co-founder Chris Larsen, alleging that they had conducted a $1.3 billion unregistered securities offering through the sale of XRP. The SEC’s position was that XRP should be classified as a security under US law, while Ripple maintained that XRP is a digital currency independent of the company.4,6

The SEC lawsuit triggered widespread consequences. Major exchanges, including Coinbase, suspended or delisted XRP trading in the United States, and the token’s price experienced significant volatility. The case became a focal point for the broader crypto industry, with many seeing it as a test of how US securities laws would apply to digital assets. Ripple mounted a vigorous legal defense, arguing that the SEC had failed to provide clear regulatory guidance and that its actions were inconsistent with how other cryptocurrencies had been treated.

In July 2023, the legal landscape shifted when a federal judge ruled that programmatic sales of XRP on public exchanges did not constitute securities transactions, while institutional sales directly to investors did. This partial victory for Ripple was celebrated across the crypto community as a key precedent, though the case did not end there. Subsequent proceedings focused on potential penalties related to institutional sales and whether Ripple’s executives could be held personally liable. In October 2023, the SEC dropped its charges against Garlinghouse and Larsen, narrowing the scope of the case to corporate issues.4,5

The SEC's five-year lawsuit against Ripple concluded in August 2025 when both parties agreed to drop their appeals, resolving the case after a mixed court ruling in 2023 declared XRP a security only when sold to institutional investors, not on public exchanges. As part of the settlement, Ripple paid a $125 million civil penalty, and the lawsuit's end provides legal clarity for the XRP cryptocurrency in the US.5,7

The case has influenced how regulators, companies, and courts approach the classification of digital assets. It also prompted Ripple to diversify internationally, expanding its operations and partnerships outside the US while continuing to push for regulatory clarity at home. Over more than a decade, these legal battles have been as central to Ripple’s story as its technological and business milestones.

Network Activity

Since the network’s inception, transaction activity has steadily grown to nearly 2.5 million transactions per day, with several noticeable spikes along the way. Although the XRPL supports many different transaction types, the majority of activity on the network consists of Payment transactions, which are used to transfer XRP or issued tokens from one account to another. Activity has generally trended higher regardless of token price, though it tends to accelerate during price increases. From January 2013 to December 2023, transactions per day rarely breached 1.0 million but in the past year transactions have averaged closer to 1.5 million per day.

Adding to transaction activity, Ripple Labs has also issued a stablecoin in 2024, RLUSD, as part of Ripple’s broader effort to expand and support global payments through DeFi use cases on the XRPL. Each RLUSD stablecoin token is pegged 1:1 to the US dollar, fully backed by US dollars or short-term US treasuries held in reserve. As of October 2025, RLUSD holds a circulating supply of $788 million, according to rwa.xyz. In comparison, Tether’s USDT and Circle’s USDC stablecoins hold a circulating supply of $180 billion and $76 billion, respectively.

Transaction fees on the network have remained consistently low, averaging pennies on the dollar for most of the network’s history. Additionally, the XRPL has had a token burn mechanism built in since its launch in 2012. From the very beginning, every transaction on the network has required a small XRP fee, and unlike some cryptocurrencies where this fee is paid to market participants like validators or miners, this fee is permanently destroyed (burned). This mechanism was designed to prevent spam attacks on the network and to make XRP slightly deflationary over time, since the total supply of 100 billion tokens can only decrease, never increase.

Active and unique addresses are key metrics for assessing a network’s fundamental value under Metcalfe’s Law, which holds that a network’s value is proportional to the square of its connected users (n²). Daily active addresses (DAAs), which measure the number of unique wallet addresses that are active on a blockchain within a 24-hour period, slowly increased in a step wise function over most of the first few years since the network’s launch. Since 2021, DAA rose sharply alongside price, then stabilized between 25,000 and 50,000, with occasional spikes in activity, corresponding to rises in token price.

.png)

Two other crypto native valuation metrics include the network value to estimated on-chain daily transactions (NVT) ratio and the market capitalization divided by the realized capitalization (MVRV) ratio.

The NVT ratio compares a network’s market capitalization to its daily transaction volume, similar to how the price-to-earnings (P/E) ratio is used in equities. It measures how much value the market assigns to a blockchain relative to the amount of value being transferred through it. A high NVT may indicate the network is overvalued compared to its usage, while a low NVT suggests stronger transaction activity relative to market cap.

Inflection points in NVT can be leading indicators of a reversal in an asset’s value. An uptrend in NVT often suggests an asset is overvalued based on its economic activity and utility, which should be seen as a bearish price indicator, whereas a downtrend in NVT suggests the opposite. The XRP NVT ratio has continuously declined since 2015 and has recently oscillated between 3 and 40. Overall, an NVT profile such as this suggests a continued increase in transactional activity relative to network value since 2015.

The MVRV ratio compares a network’s current market capitalization (based on the latest trading price) to its realized capitalization (the value of all coins at the price when they last moved on-chain). This ratio helps assess whether a cryptocurrency is overvalued or undervalued relative to the cost basis of its holders. A high MVRV often signals that investors are sitting on large unrealized gains, which can precede profit-taking and market corrections, while a low MVRV suggests coins are trading closer to or below their holders’ cost basis, potentially indicating undervaluation or accumulation opportunities.

Since 2018, XRP’s MVRV has ranged between 0.5 and 2.5, typically climbing toward the upper end of that range alongside rising XRP prices. XRP currently holds an MVRV just under 2.0, near multi-year highs, suggesting an elevated level of unrealized gains relative to the previous seven years.

%20(2).png)

Another useful sentiment metric for cryptocurrencies is Google Trends, which measures search activity of a given subject. Sudden rises or spikes in Google trends often correspond with rises in price and correlate with trading volumes. Divergences in search vs price action can also suggest pending price activity, both up and down.

Worldwide Google Trends data for the term “XRP” reveals significant search activity in late 2024, corresponding to a rise in price at that time. Searches have cooled off but remained elevated over the past year, higher than any prior period since 2020. The search spike in 2025, mirrored the July price spike when XRP saw a new all-time high. A lower high in searches with a higher high in XRP price was an example of a bearish divergence in search interest relative to price. If price reaches a new all-time high, search interest will also need to surpass its July 2025 peak to avoid forming a bearish divergence.

XRP - The Bridge Currency for Global Finance

XRP, launched in 2012 by Jed McCaleb, David Schwartz, Arthur Britto, and Chris Larsen and originating from Ryan Fugger’s RipplePay concept, is a digital asset with a fixed supply of 100 billion tokens that powers the XRP Ledger (XRPL) for fast, low-cost, and scalable transactions. Its primary use case is as a bridge currency for cross-border payments via RippleNet and On-Demand Liquidity (ODL), adopted by institutions such as SBI Remit, MoneyGram, Santander, and Tranglo, while retail adoption is supported by BitPay and a growing XRPL ecosystem including decentralized exchanges, NFTs, and tokenization projects. XRP’s supply is managed through fixed issuance, a cryptographically secured escrow system, and controlled programmatic and institutional sales, ensuring predictable distribution and liquidity. Ripple has navigated significant legal challenges, most notably the SEC lawsuit, which concluded in August 2025 with a $125 million civil penalty and XRP recognized as a security only in institutional sales, providing regulatory clarity in the US.5 The XRPL continues to see high network activity with thousands of transactions per second, supporting a robust ecosystem and cementing XRP’s role as a distinctive asset in global payments.

Sources

Risks & Disclosures

XRP is subject to unique and substantial risks, including significant price volatility and lack of liquidity and theft. XRP is subject to rapid price swings, including as a result of actions and statements by influencers and the media, changes in the supply of and demand for digital assets, and other factors. There is no guarantee that XRP will maintain its value over the long-term.

The statements, views, and opinions expressed herein are those of the Canary Capital Group LLC. The information presented is derived from sources the Firm believes to be reliable; however, the Firm makes no representation or warranty as to the accuracy, completeness, or timeliness of such information. The digital asset landscape is rapidly evolving, and information provided may change over time without notice.

This site is for informational purposes only.

This information within it is not intended as an offer to sell, or the solicitation of an offer to buy any securities. Such offerings may only be made by prospectus and offering documents. Carefully consider the risk factors, investment objectives, fees, expenses, and other information associated with before making an investment decision. All investments are speculative, may be illiquid and involve a high degree of risk, uncertainty, and there is risk of the complete loss of the investment. There is no guarantee that any specific outcome will be achieved. We do not offer tax, financial, accounting or legal advice. The summary set forth on this website does not purport to be complete, and is qualified in its entirety by reference to the definitive offering documents.

The materials on this website or any third-party websites accessed herein are not associated with and have not been reviewed or approved by: (i) Canary Capital Group LLC or the products sponsored by Canary Capital Group LLC; or (ii) the marketing agent of Canary Capital Group LLC’s products. Each of the above hereby disclaim any and all information, products, or services described on this website or any third-party website accessed herein.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of positing, and are subject to change without notice. The information and opinions are derived from proprietary and non-proprietary sources deemed to be reliable, are not necessarily all-inclusive, and are not guaranteed as to accuracy. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

This material is published in good faith but no advice, representation or warranty, express or implied, is made by us or by any person as to its adequacy, accuracy, completeness, reasonableness or that it is fit for your particular purpose, and it should not be relied on as such. This material does not purport to be complete and is subject to change. You acknowledge that certain information contained in this website supplied by third parties may be incorrect or incomplete, and such information is provided on an "AS IS" basis. We reserve the right to change, modify, add, or delete, any content and the terms of use of this website without notice.

No information on this website constitutes business, financial, investment, trading, tax, legal, regulatory, accounting or any other advice. If you are unsure about the meaning of any information provided, please consult your financial or other professional adviser.

Investment involves risks. Past performance is not a guide to future performance. The value of investments and the income from them can fall as well as rise and is not guaranteed. You may not get back the amount originally invested. Any strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

This website has not been, and will not be submitted to become, approved/verified by, or registered with, any relevant government authorities under the local laws. This website is not intended for and should not be accessed by persons located or resident in any jurisdiction where (by reason of that person's nationality, domicile, residence or otherwise) the publication or availability of this website is prohibited or contrary to local law or regulation or would subject us to any registration or licensing requirements in such jurisdiction.