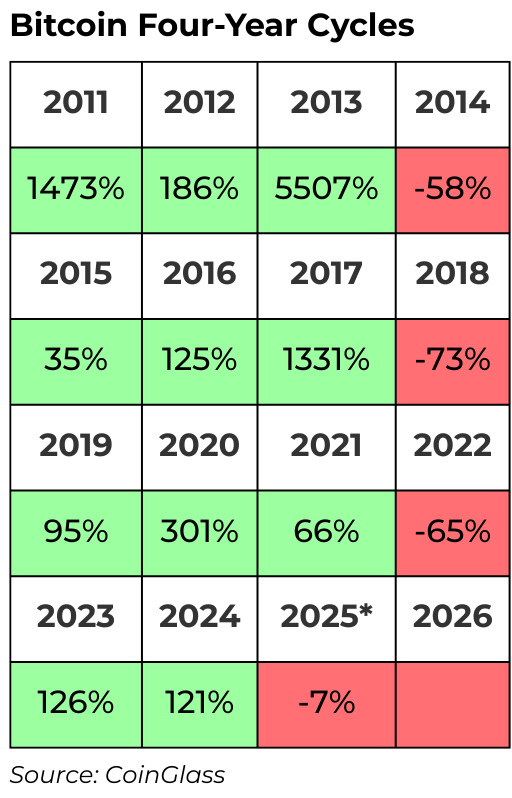

Bitcoin's Four-Year Cycle: The 2025 Reality Check

.png)

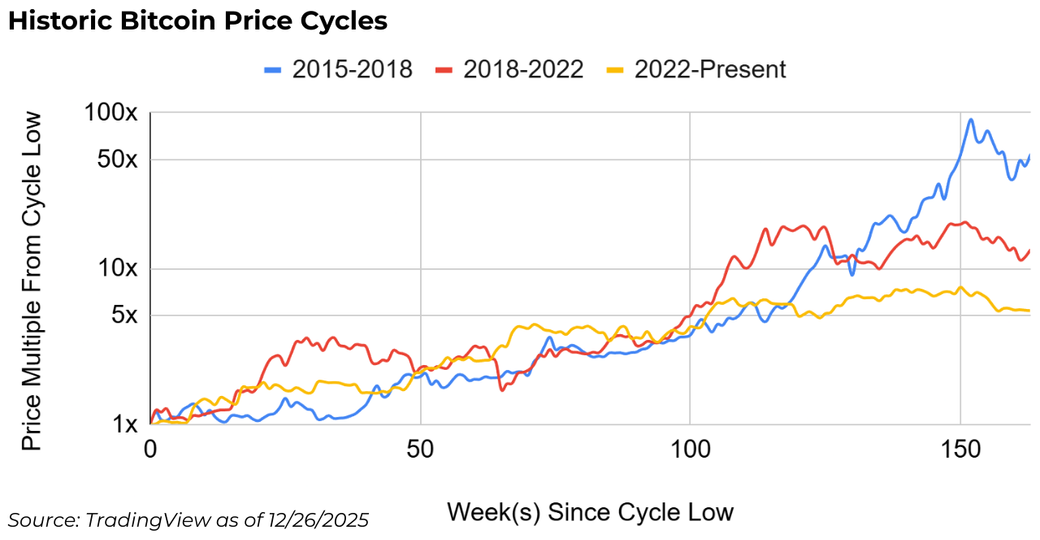

Bitcoin’s Four-Year Cycle & the 2025 Selloff

Bitcoin’s four-year cycle remains fundamentally driven by miner behavior, specifically, the need to sell BTC to fund electricity costs, capital expenditures, expansion, and to manage balance-sheet risk ahead of the traditional “bear year.” Historically, miners tend to sell in coordination: once selling pressure begins, few want to be the last to de-risk, leading to cascading supply.

In this cycle, however, the selloff occurred earlier than expected due to two key catalysts: rising energy costs and the collapse of the basis trade.

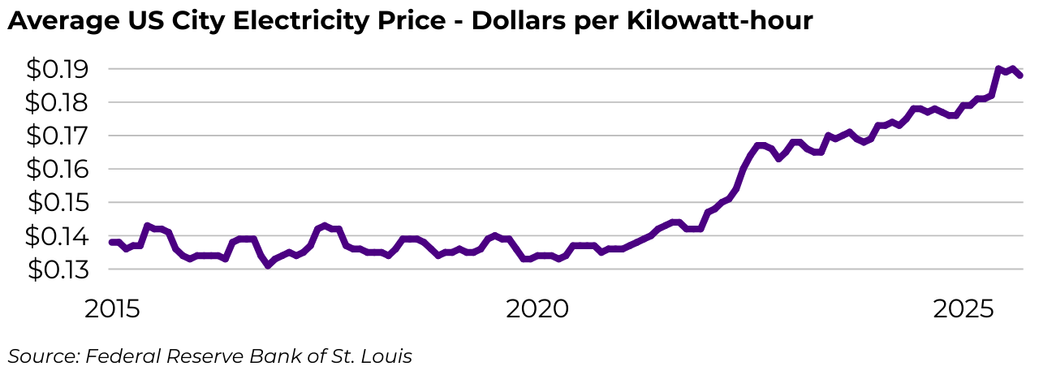

Catalyst One: Rising Energy Costs

The first catalyst was a sharp increase in electricity costs, driven by the rapid expansion of AI data centers. While some large miners benefit from fixed-rate contracts or operate as energy intermediaries, the majority of small and mid-sized miners are exposed to variable pricing. Energy rates rose meaningfully over the summer, forcing many miners to liquidate BTC holdings. This resulted in widespread miner capitulation earlier in the cycle than historical norms.

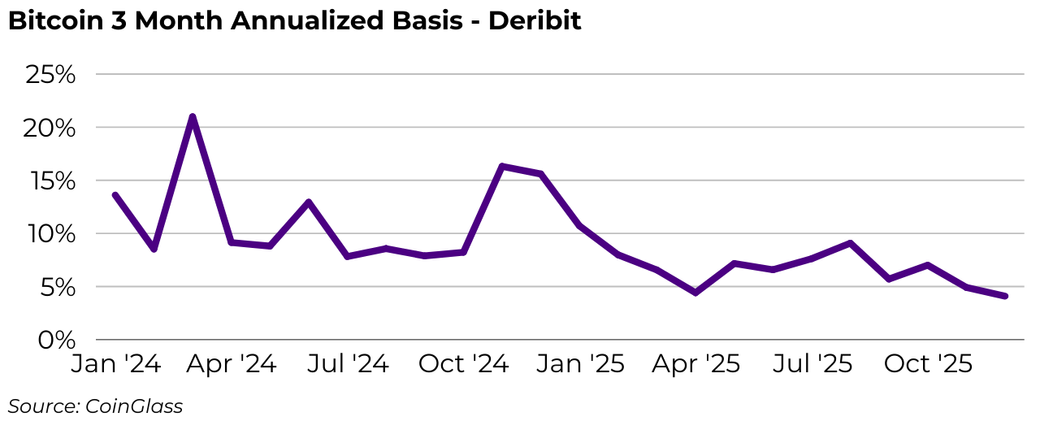

Catalyst Two: Collapse of the Basis Trade

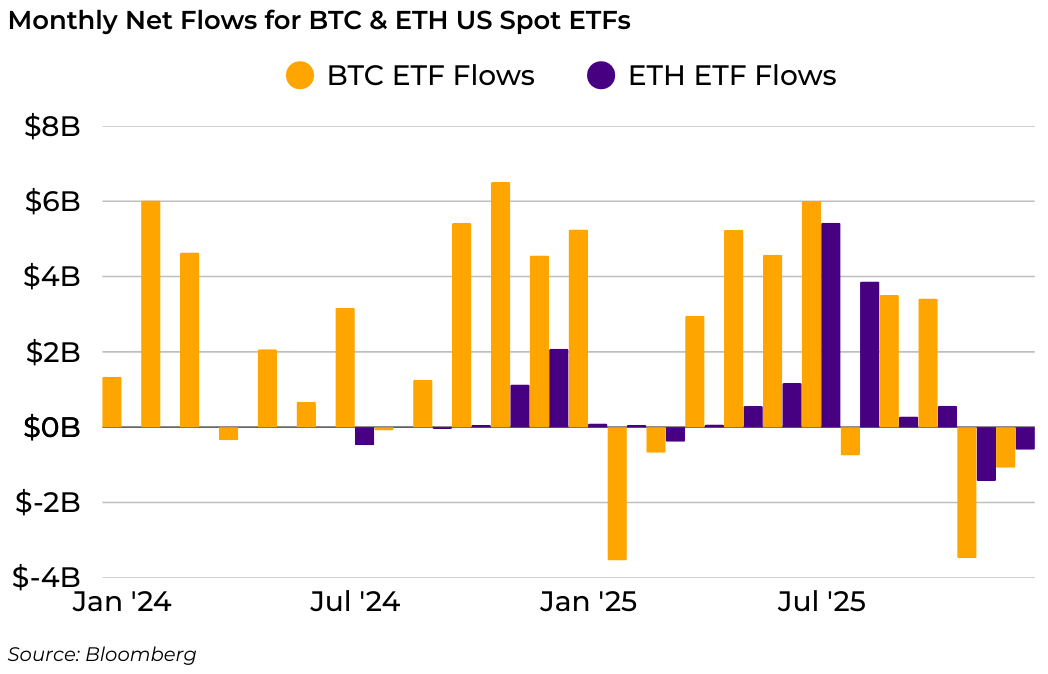

The second catalyst was the unwinding of the Bitcoin basis trade. Historically, Bitcoin futures traded at elevated premiums due to fragmented and inefficient markets. However, following the launch of Bitcoin ETFs two years ago, market efficiency improved substantially. The compression of the futures–spot spread rendered the basis trade unattractive, prompting traders to unwind positions by selling ETF exposure. These ETF outflows applied additional downward pressure on BTC prices and further exacerbated miner capitulation.

Is the Four-Year Cycle Broken?

Some market participants argue that the four-year cycle is broken, citing:

- The absence of a traditional blow-off top

- Increased institutional participation via ETFs

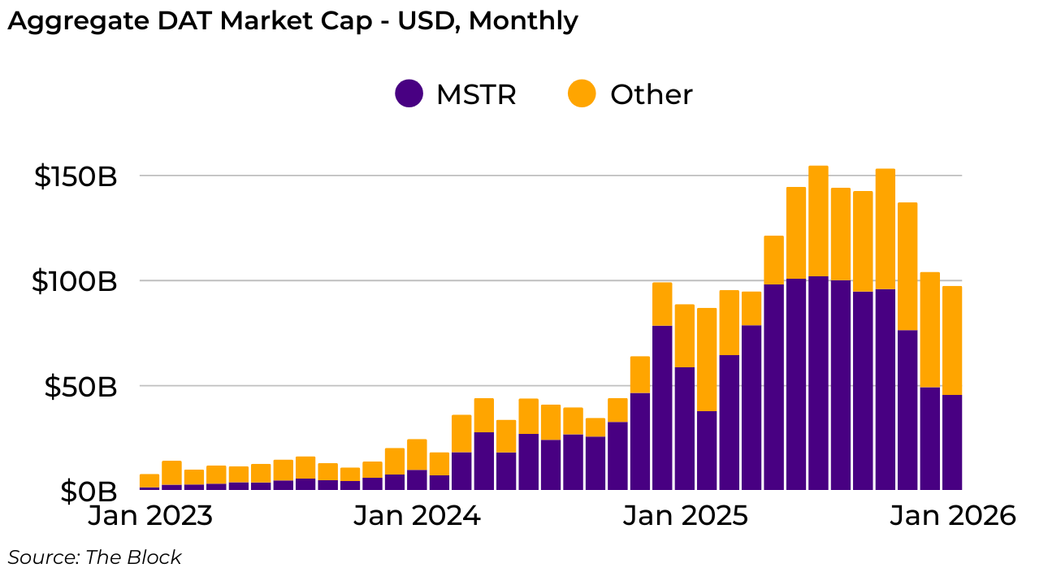

- The rise of Digital Asset Trusts (DATs)

- Ongoing global monetary expansion

I disagree. The four-year cycle remains intact. Bitcoin peaked in October at approximately $126,000, consistent with prior cycle timing. That said, my 2025 price target of $140,000 was incorrect. I overweighted Bitcoin’s correlation with global M2 money supply and underweighted two critical dampening forces: the collapse of the basis trade and the surge in demand for gold.

Throughout most of 2025, weak consumer spending and deteriorating sentiment kept me skeptical of a blow-off top. Those types of finales typically require a late surge from retail investors, and that dynamic simply wasn’t present, retail lacked the excess capital needed to pile in (more on this later).

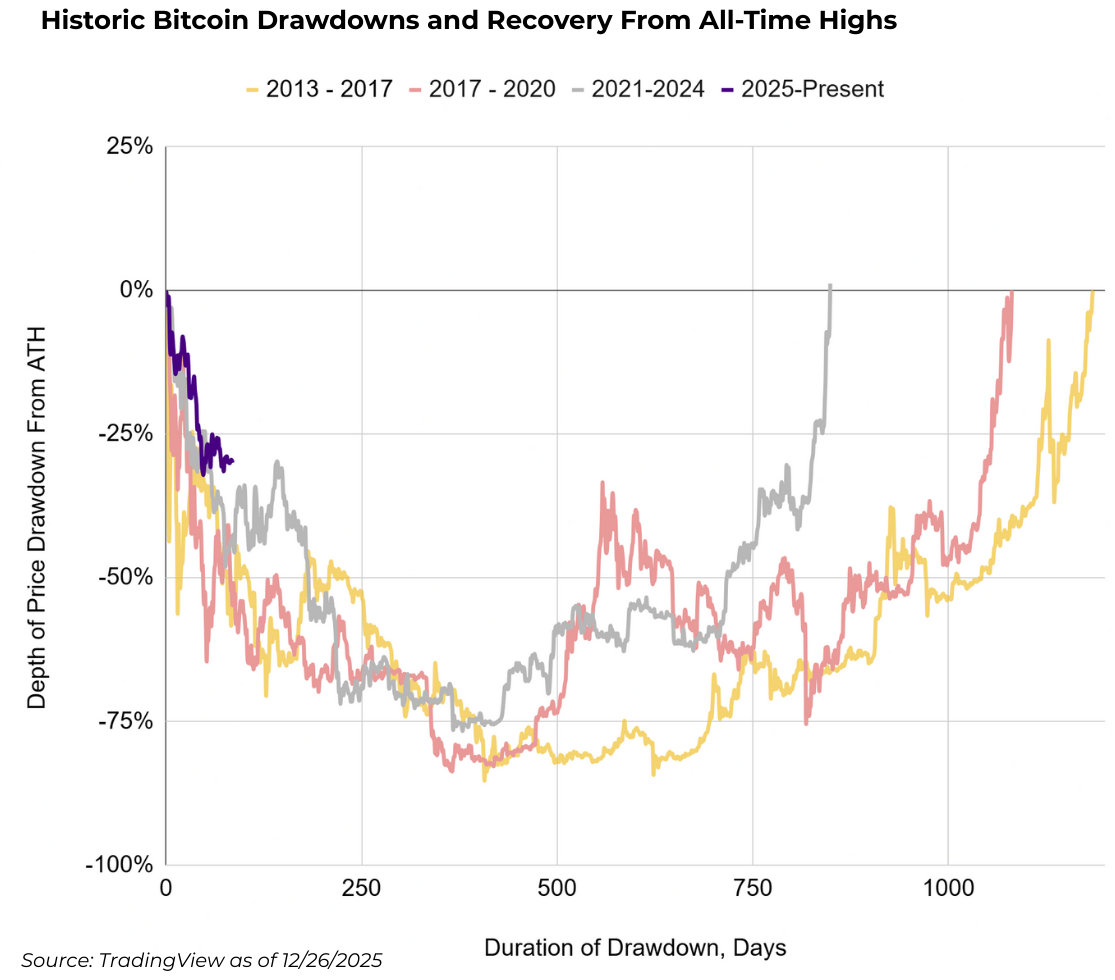

A third factor was the Binance disruption on October 10, 2025. While Binance itself was not the root cause, the event accelerated the cycle’s conclusion by triggering large-scale liquidations and eliminating the traditional blow-off top. Historically, cycle peaks occurred in November 2021, December 2017, and December 2013, followed by approximately nine months of mean reversion before a new all-time high roughly one year later.

But the Institutions Are Coming. Are Miners Still Relevant?

The claim that ETFs and DATs will unlock enough new institutional and retail capital to eliminate the role of miners is simply not true, at least not this cycle. Over the long term, perhaps, but not now. While improved access has increased demand across investor classes, behavior matters just as much as availability.

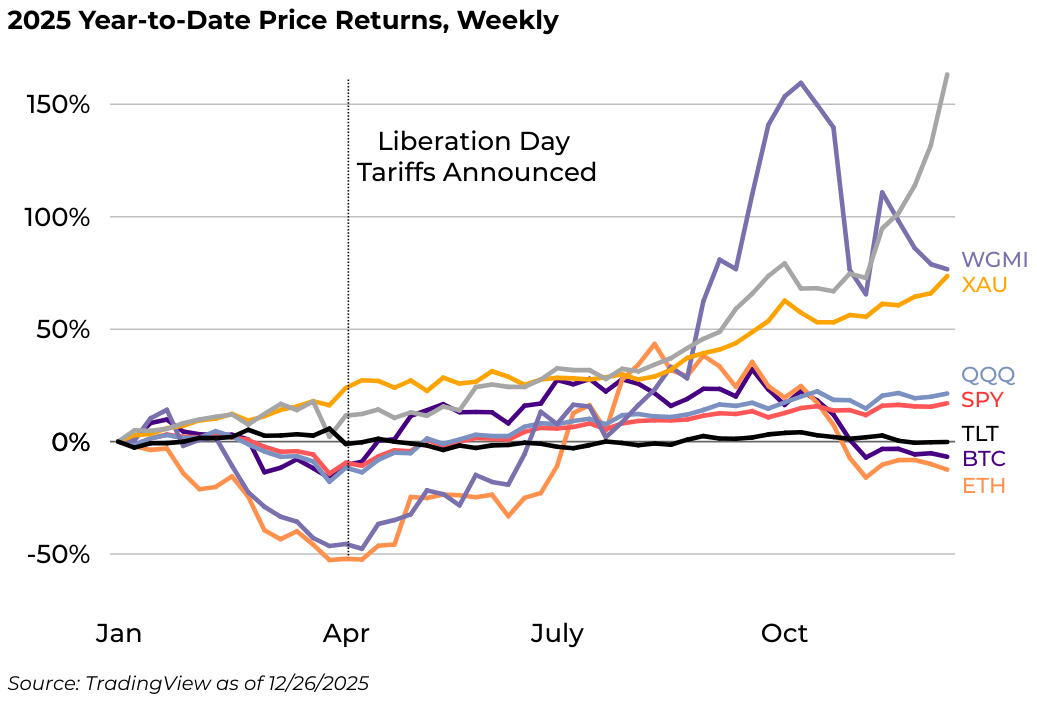

Consider how retail investors and financial advisors typically respond. At the time of writing, Bitcoin is down roughly 6% year over year. That makes it an attractive candidate for tax-loss harvesting, especially for investors sitting on gains elsewhere, equities are up about 20% YTD, and gold has delivered gains of more than 70%. When retail investors are holding a losing position while the broader market is rising, they tend not to re-enter quickly.

Financial advisors face similar constraints. Those with set Bitcoin allocations may delay next year’s rebalance until they better understand why Bitcoin underperformed equities. In the meantime, capital stays sidelined. Smart money, however, is simply waiting for the right entry point.

DATs are revealing the true state of the market. Think of them as expensive, closed-end funds. These publicly traded companies were approached by investment banks to create structures that hold digital assets on their balance sheets. Most of these firms were already in weak financial positions—typically unprofitable, with strained balance sheets and high debt-to-equity ratios, leaving them few refinancing options in a high-interest-rate environment.

To execute the strategy, DATs raised PIPE capital from hedge funds, issuing new shares and using the proceeds to purchase various cryptocurrencies. Once those shares were issued, PIPE investors quickly sold them in the open market and moved on to the next opportunity. Beginning in August, however, there were no longer enough buyers on the other side. As a result, many DATs now trade at roughly 50% discounts to NAV, indicating that effective demand is only half of underlying supply.

The economics of these structures are also deeply inefficient. Launching a PIPE and maintaining a digital asset treasury is expensive, unnecessarily so. Investment banks typically take around 7%, legal fees run another 3%, and warrants are granted to larger investors as additional incentives. That means investors often start with an immediate ~10% loss. On top of that, many companies issue warrants and generous compensation to management and new board members, while hiring external asset managers to oversee the crypto at fees ranging from 1–5%.

Worse still, because many of these operating businesses continue to lose money, they effectively bleed the digital treasury to fund day-to-day operations. In practice, this is like buying a crypto ETF that loses 10%+ on day one and then charges 5%+ in annual fees. But we digress.

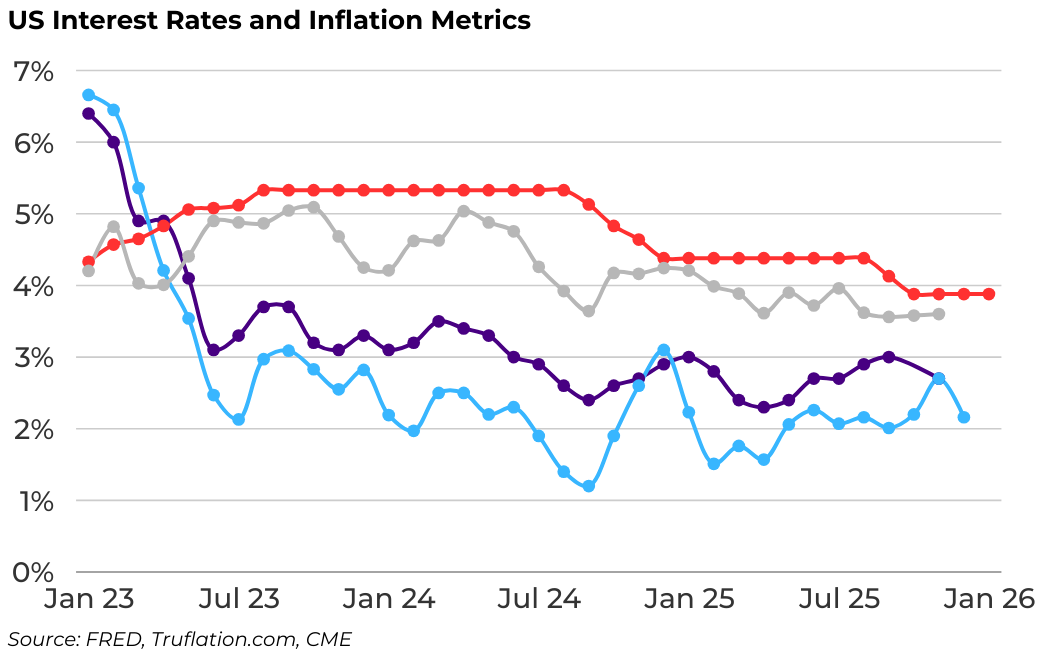

Macro Backdrop and Policy Implications

The US is shifting toward a dovish monetary stance, though it is essentially playing catch-up while Japan tightens policy. Historically, each time the BOJ raises rates, Bitcoin prices tend to decline. Meanwhile, much of the rest of the world is likely to maintain or adopt dovish policies.

The rationale for these dovish expectations is slow global growth and recessionary pressures in many countries. Central banks may inject liquidity to support banks, corporations, and investors with capital to deploy. However, most of the population continues to struggle after years of high inflation and low growth.

Looking ahead, a new Fed Chair in 2026 may not achieve the intended market impact by the end of summer, setting the stage for the next four-year economic and market cycle.

Drawdowns, Halvings, and the Path Forward

Each halving cycle delivers diminishing marginal impact, but forced sellers, particularly miners, remain structurally influential. Both upside and downside volatility have moderated with each cycle. I expect this bear phase to result in a 50–55% peak-to-trough decline. With BTC already down roughly 30%, a gradual decline over the next 6–9 months is reasonable. This trajectory aligns with expected Federal Reserve policy shifts and suggests a cyclical trough forming in mid-to-late summer, followed by recovery.

What Investors Should Watch Next

2026 is likely to be defined by adoption and real business profitability, with emphasis on on-chain lending and borrowing, tokenization of real-world assets and stablecoins & payments infrastructure

While Bitcoin remains a dominant macro driver, meaningful short-term divergences are likely as blockchain-based businesses mature.

- XRPL is emerging as a dominant financial-services rail and is increasingly recognized by institutions. I expect upside divergence.

- Hedera (HBAR) continues to lead in enterprise-focused infrastructure, with strong fundamentals heading into 2026.

- Privacy assets remain underappreciated. Litecoin’s optional privacy features, driven by Charlie Lee’s long-term vision, are likely to gain relevance as regulatory and transactional privacy become focal points.

- There will be more users of Monero, Canton, and Litecoin, with continued price divergence.

- Tokenization and stablecoin platforms will continue to expand. While ETH and SOL remain leaders, we are closely monitoring SUI, SEI, and INJ as they move up the adoption curve, each offering meaningful upside potential.

Disclaimer

Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. The opinions expressed in the newsletter may change without notice. Any views or opinions expressed in the newsletter may not reflect those of the firm as a whole. The information in our newsletter may become outdated and we have no obligation to update it. The information in our newsletter is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. It is provided for information purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security or investment. No recommendation or advice is being given as to whether any investment is suitable for a particular investor or a group of investors. It should not be assumed that any investments in securities, tokens, sectors or markets identified and described were or will be profitable. We strongly advise you to discuss your investment options with your financial adviser prior to making any investments, including whether any investment is suitable for your specific needs.