Digital Asset Resilience Meets a Critical Macro Week

Key Takeaways

- BTC and ETH are both near key price levels amid strong institutional interest

- Seasonal trends may take a back seat to post-halving strength and liquidity

- Event-heavy week ahead with earnings from tech giants and key economic data

Digital Asset Commentary

Bitcoin continues to trade within a tight range. As of last Friday, Galaxy Digital announced the completion of an 80,000 BTC sale from a long-term holder dating back to 2011. Meanwhile, Michael Saylor’s latest preferred stock IPO, STRC, raised $2.52 billion, making it the largest IPO of the year at more than twice the size of Circle’s. The proceeds will be used to purchase additional BTC in the coming days. The key BTC breakout level remains $120k, with a Cup and Handle bullish continuation pattern suggesting a potential target range of $140k to $160k. Ethereum has also quickly approached a key psychological level of $4,000, with multiple treasury companies set to continue buying ETH at a voracious pace. A BTC breakout to new all-time highs may be enough to also provide ETH with its first all-time high since October 2021, which currently stands at $4,878

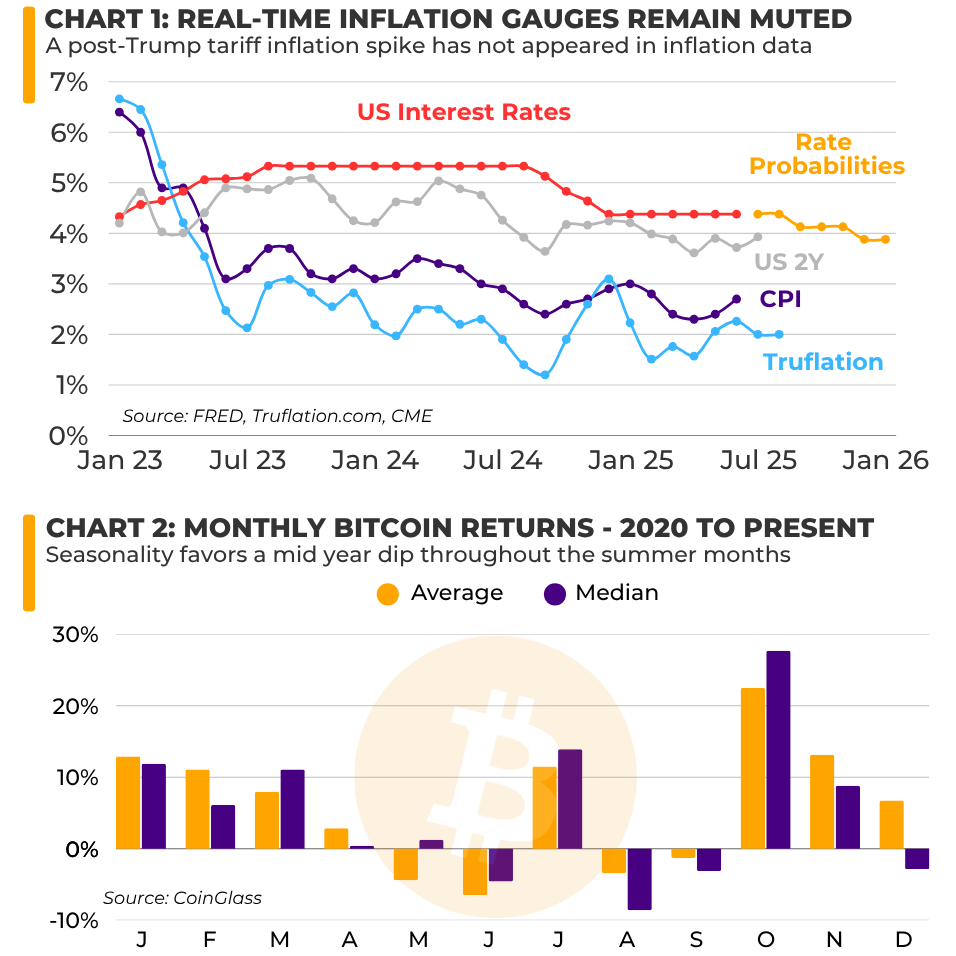

Despite recent bullish momentum, especially from Ethereum, seasonally bearish months lie ahead. Historically, BTC underperforms in August and September before strong Q4 rallies. However, in post-halving years, August has averaged a 36% gain since 2013, contradicting the usual trend. With legacy indices pushing all-time highs on low volatility and traditional safe havens like gold remaining subdued, digital assets may have room to move higher.

This week, markets face a packed calendar. Major earnings reports from Microsoft, Apple, Amazon, and Meta are on deck, alongside the Federal Reserve’s interest rate decision, where no change is expected. The Treasury’s Quarterly Refunding Announcement (QRA) will reveal the updated financing estimate and the planned mix of bills versus bonds. Key macroeconomic data, Q2 GDP, the July jobs report, and the PCE inflation gauge, will be released throughout the week. On Friday, Trump is expected to issue new tariff letters, following finalized trade deals with Japan and the EU last week. Any one of these events or data releases could spark volatility in a market that hasn’t seen a single-day move of more than 2% in the S&P 500 since May 26th.

Download Commentary

Download Commentary