Seasonality & Futures Positioning Signal Crypto Headwinds

Key Takeaways

- BTC & ETH seasonality points to flat-to-down Q3, rebound in Q4

- ETH futures positioning bearish, historically the more reliable side of the trade

- MSTR trades at 1.42x mNAV; ATM for BTC buys or arbitrage risk if premium persists

Digital Asset Commentary

Momentum in both BTC and ETH has stalled near record highs, with ETH still below its last all-time high from Q4 2021. Despite billions in inflows via ETFs and corporate treasuries, ETH’s 250% rally since the April low may require a prolonged consolidation before another leg higher. Seasonality for both BTC and ETH suggests a flat-to-down Q3, followed by a stronger Q4 rebound.

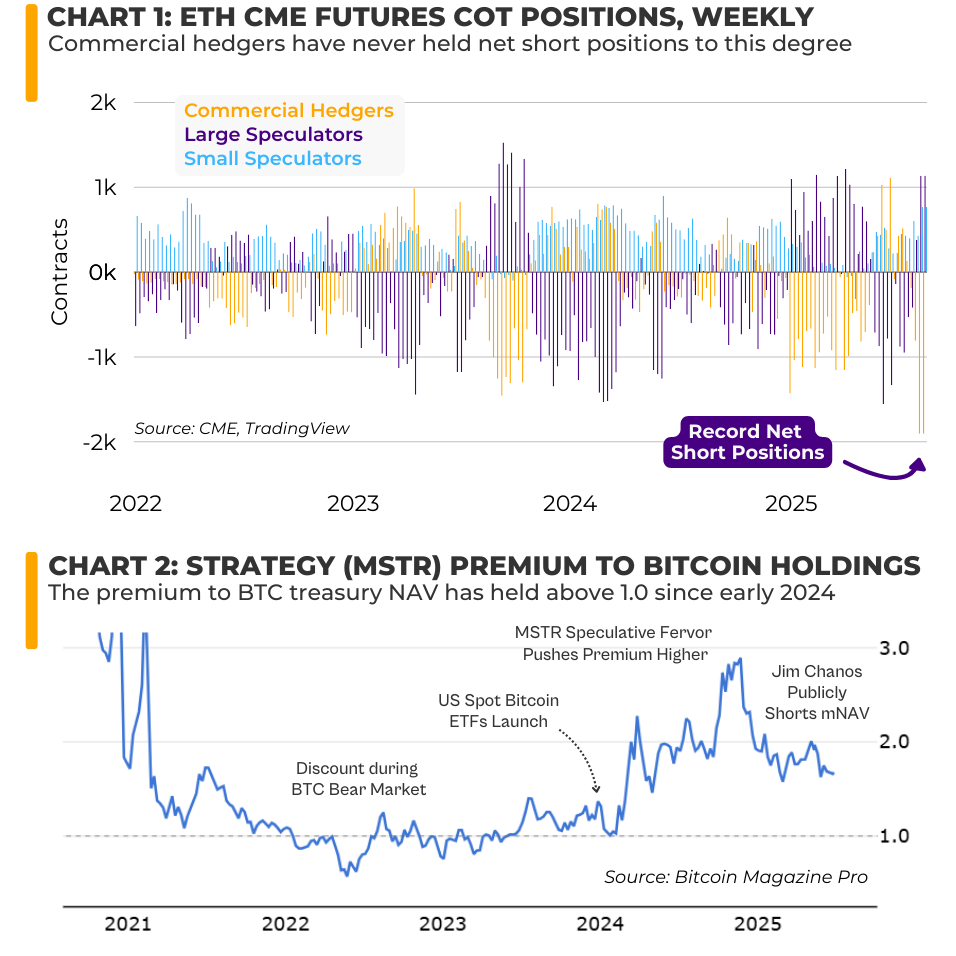

ETH CME Futures Commitment of Traders (CoT) data adds to the bearish case. Commercial hedgers now hold a record net short position, which has risen sharply in recent weeks. Historically, commercials tend to position correctly, while large speculators and retail investors often represent the crowded side of the trade.

On the BTC side, MicroStrategy (MSTR), the largest corporate holder, has slowed purchases in recent weeks while still trading at a premium to its BTC holdings (mNAV). Proponents argue this premium reflects liquidity advantages versus native BTC markets, the use of leverage through debt, scarcity of pure-play BTC equities, and optionality for future BTC acquisitions.

That premium currently sits around 1.42x, down from a 3.41x peak in November 2024. As long as it remains above 1.0x, further BTC buys via the at-the-market (ATM) program are likely. If the premium widens, short-MSTR/long-spot BTC pair trades become increasingly attractive as an arbitrage play. On the last earnings call, Saylor suggested MSTR would avoid ATM issuance below a 2.5x premium, but has since softened that stance, noting the company may issue below that level if advantageous. If MSTR doesn’t act to narrow the premium, as Jim Chanos has argued, the market eventually will.

Download Commentary

Download Commentary