Where Has the Liquidity Gone?

A market observer I follow recently noted that most small-cap cryptocurrencies are down roughly 90% from a year ago. His framing was relative value. Ours is risk. This stage of the cycle historically separates durable networks from speculative excess. The former survive and consolidate; the latter trend toward irrelevance.

More broadly, crypto markets experienced a sustained liquidity drain throughout 2025. For readers who prefer the conclusion upfront: there is little reason to expect a material liquidity rebound in 2026.

Exchange Volume: A Broad-Based Decline

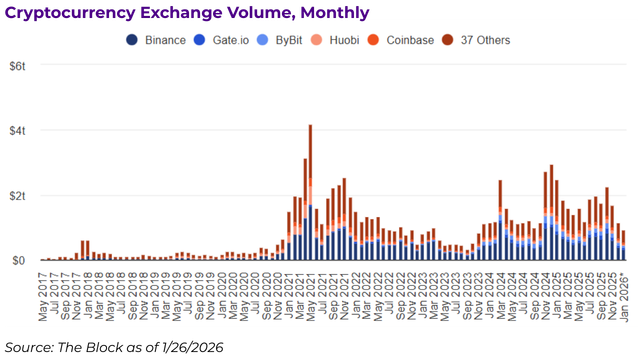

We begin by examining trading volume across major exchanges to determine whether the contraction is retail-driven, region-specific, or structural.

After reviewing both US and non-US venues, the pattern is clear: volume has declined across the board since the post-election peak following President Trump’s victory. There is no meaningful geographic divergence. This suggests a global reduction in risk appetite rather than localized regulatory or access issues.

Historically, crypto bull market peaks, particularly within the four-year cycle framework, are accompanied by peaks in trading volume. While the October 2025 price high did see a modest uptick in volume, it failed to reach the levels observed in November through January of the prior year. In other words, price advanced without broad participation.

Macroeconomic conditions help explain why. Consumer debt delinquencies and defaults across multiple categories are at their highest levels since the Global Financial Crisis. When households are struggling to service credit card balances, discretionary capital for speculative assets such as crypto is naturally constrained.

Why Crypto Is Not “Next” in 2026

Some market participants point to strong performance in gold, silver, and equities as evidence that crypto is merely lagging and will “catch up” in 2026. We disagree, for several reasons:

Precious metals are increasingly serving as alternatives to sovereign debt for both central banks and institutional investors seeking safety and neutrality.

- Equities continue to benefit from persistent institutional inflows and structural demand from passive vehicles, buybacks, and pension allocations. Crypto, by contrast, remains categorized as a higher-risk allocation and commands smaller portfolio weights.

- Hedge fund positioning has shifted materially. In 2025, many funds reduced exposure to Bitcoin and Ethereum as the futures basis trade collapsed. Capital rotated primarily into bonds and equity indices, but also into alternative digital assets such as XRP, SOL, and HBAR following the launch of ETFs tied to those assets. This dynamic explains both outflows from BTC and ETH ETFs and concentrated inflows into newer products.

- Relative performance matters. Equities and precious metals are catching up to crypto’s outsized gains from 2023 and 2024, not the other way around.

A Structural Shift in Sentiment

Retail investors still have capital, so why has participation declined so sharply?

First, crypto is widely perceived as having already delivered its major gains this cycle, with limited upside remaining relative to risk. Second, the market increasingly feels like an insiders’ game. Repeated liquidations, opaque mechanics, and asymmetric information have eroded retail confidence in their ability to generate durable edge.

At the same time, capital is migrating toward prediction markets, which many retail participants view as more transparent and less manipulable. Platforms such as Kalshi and Polymarket have seen rapid volume growth. Notably, major exchanges appear to have recognized this shift in real time: Coinbase, Gemini, and Crypto.com have all launched prediction market offerings, opting to adapt rather than risk obsolescence, an outcome reminiscent of legacy media’s response to streaming.

ETFs and the Changing Role of Exchanges

We have long argued that the introduction of spot ETFs fundamentally alters the role of crypto exchanges. As ETFs proliferate, exchanges increasingly resemble custodial and on-ramp infrastructure rather than primary venues for speculative trading.

For many investors, paying tens of dollars in brokerage commissions is preferable to paying hundreds, or more, in exchange trading fees. This shift is already visible. In our own experience, exchange fees in 2025 ran into the thousands of dollars, accelerating the move toward brokerage-based trading as ETF access expanded.

Exchanges are responding accordingly. Kraken, for example, has expanded into securities trading, reflecting the reality that crypto-native platforms must diversify as asset exposure migrates into traditional financial rails.

What This Means Going Forward

Retail participation has largely exited, leaving crypto increasingly institutional in nature. That has implications:

- Capital will concentrate in protocols tied to real-world asset tokenization, regulated financial infrastructure, and demonstrable revenue models.

- Speculative meme assets and low-utility tokens face continued attrition. Assets down 90% are not “cheap”; many will decline another 90%.

- Market focus will narrow to assets with ETF access, liquid futures markets, and real economic activity, regardless of whether those businesses are centralized or decentralized.

This is not a temporary pause. It is a structural transition. The market of 2026 will look smaller, more concentrated, and more selective, and for most legacy speculative tokens, far less forgiving.

Disclaimer

Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. The opinions expressed in the newsletter may change without notice. Any views or opinions expressed in the newsletter may not reflect those of the firm as a whole. The information in our newsletter may become outdated and we have no obligation to update it. The information in our newsletter is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. It is provided for information purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security or investment. No recommendation or advice is being given as to whether any investment is suitable for a particular investor or a group of investors. It should not be assumed that any investments in securities, tokens, sectors or markets identified and described were or will be profitable. We strongly advise you to discuss your investment options with your financial adviser prior to making any investments, including whether any investment is suitable for your specific needs.